City's Improper Tax Billing for Properties Under Appeal

With no improvements to the property itself, my appraised property value increased by almost 25% this year. So, like many other Sugar Hill taxpayers, I appealed the 2023 property value.

Property tax appeals are subject to various state laws and take a while to process. With an increased volume of appeals - like Gwinnett and surrounding counties are seeing this year - it’s taking even longer.

While I await the final value, Gwinnett County billed me using last year’s property value. After the value is finalized, I’ll be billed for any additional taxes due. Seems fair.

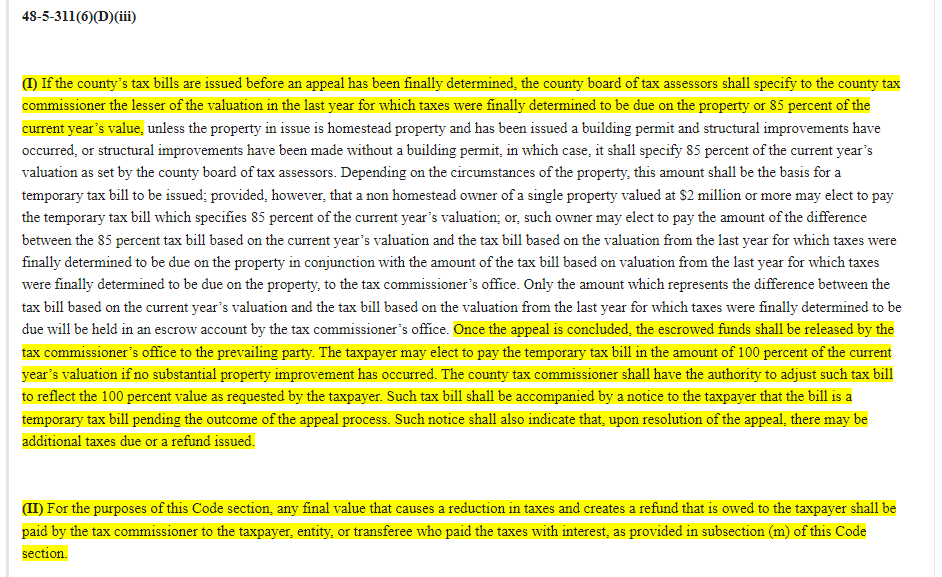

I reached out to the Gwinnett County Tax Assessors office to ask if this was a County policy, or if there was a state law that governed the tax billing of properties under appeal. My ever-helpful contacts directed me to the statute they use, OCGA 48-5-311 (e)(6)(D)(iii)(I), which says that for unimproved properties under appeal, the county tax assessors must temporarily set the property value at either 85% of the new value or at the previous year’s value, whichever is less.

According to that statute, the tax commissioner can adjust the bill to use the new, higher value at the request of the taxpayer.

At the conclusion of the appeal, the taxpayer is either billed for any additional taxes due, or issued a refund.

You’ll notice that this applies to the counties, but cities are not specifically mentioned. The counties are the ones who do the property appraisals.

OCGA 48-5-352 (a) indicates that the municipalities get their value from the counties and should use that value.

Former Mayor Gary Pirkle’s property value increased by more than 78% this year, so he also appealed. His appeal, like mine, is still underway. He told me that the City of Sugar Hill billed him using the new, inflated property value that he was appealing. I looked at my bill, and saw they’d done the same thing to me. This was in stark contrast to the fair and clear property tax billing procedures followed by Gwinnett County.

Gary reached out to the City Clerk, who advised him to contact the City’s Finance Director. After the October City Council meeting, Gary initiated a discussion with the Finance Director. I was present for the discussion. She informed us that this was just the City’s policy.

So, if you have a property under appeal in Sugar Hill, YOU were also billed on the full, pre-appeal amount.

Gary called one of the City’s attorneys, who declined to say much since he represents the City (as in the government, not the residents). The City attorney did say he would speak with the City and that Gary could expect a response from them.

After Gary called the attorney again, the City’s Finance Director sent him an email saying that after a conversation with the City Attorney, his bill was being changed. The amended bill used 85% of the new 2023 value.

Pirkle told them that it still wasn’t correct, because the law says the value for properties under appeal should be 85% of the current year’s value OR the previous year’s value, whichever is less.

The Finance Director responded that the City’s software could not bill at anything less than 85% of the current year’s value. However, she manually created a bill using the previous year’s value.

This adjustment to Gary’s bills seems to indicate that the City believes its policy is not legal and could cause issues. Gary asked the City in his emails if they were going to adjust everyone’s bills, and the Finance Director simply stated that she was “reviewing” them. As of November 4, I have not received an updated bill, and the bills are due on November 17.

Gary and I have been calling and researching to get an explicit, documented statement as to whether the City’s property tax billing procedure is legal, and to find out who actually enforces these laws. We consulted the Gwinnett County Tax Assessor’s Office, the Gwinnett County Tax Commissioner, the Georgia Attorney General’s Office, the Georgia Department of Revenue, the Office of the General Counsel of the Georgia Department of Revenue, and several private attorneys.

None of the government entities would explicitly say it wasn’t legal. But, no one said that it was legal. If OCGA 48-5-352 (a) could possibly be construed to allow what the City of Sugar Hill is doing, that seems like an easy answer that Gwinnett County, the Georgia Department of Revenue, or especially the City’s Attorney could have given us. Yet, none did. Furthermore, I was advised by a couple of people in government to seek the advice of an attorney. Interesting advice if there was nothing to see here.

Ultimately, the answers Gary and I received suggest that the way the City is billing property taxes is likely not completely legal, but that no government agency either has or will exercise the authority to control it. For most residential taxpayers who only own one property, it costs more to sue the City than it’s worth. So, the City takes advantage of the situation to make things easier for itself and possibly make extra money by collecting interest on the extra tax money as they hold it.

A Local Government Compliance Specialist at the Department of Revenue HAS told me TWICE now that legally, if the City bills at the higher value now and the property value is later lowered through the appeal, the City owes taxpayers a refund PLUS interest. He included a highlighted screenshot of this statute in his email to me.

It doesn’t seem likely the City will honor the law, so I followed up and asked him who enforces that. He told me that the Department of Revenue can’t do anything and that ultimately, residents will have to approach the City on their own.

He concluded with one final piece of wise - and very timely - advice:

“The ultimate enforcer of any city will be the voting booth.”